In the world of small museums, location and audience significantly influence expenses, rendering a one-size-fits-all approach ineffective. However, gaining insight into the various types of expenses museums incur can shed light on common challenges and their causes. The non-profit financial Form 990 categorizes expenses into five areas, providing a framework for understanding spending patterns. Our goal is to simplify the concept of museum spending and guide museums toward prudent budget management by exploring these key expense categories.

Decoding Expense Categories

1. Grants and Similar Amounts Paid

Museums not only receive grants, but a few also provide them. Using these funds wisely, small museums can create ripples of impact, extending their reach beyond the confines of their walls. But it’s rare and usually will be zero in most Form 990 for history-focused organizations.

2. Benefits Paid to or for Members

Resources directed towards a non-profit are sometimes redirected back to members such as with insurance benefits or patronage dividends. This is significant for organizations that exist for mutual benefit, like unions, clubs, and certain types of non-profit organizations but less so for history-focused organizations. It is important to understand that this does not encapsulate museum membership program benefits. These are exceedingly rare for history-focused organizations and usually will be zero in most Forms 990.

3. Salaries, Other Compensation, Employee Benefits

The staff of a museum is its beating heart. Ensuring their compensation is both fair and sustains talent is a testament to a museum’s commitment to its mission. This significant expense will exist for all history-focused organizations and can typically exceed half of all expenses.

4. Professional Fundraising Fees

Fundraising, when done deliberately, can be transformative. It’s an investment that pays dividends in the form of donations and grants, fueling the museum’s ambitions. Enlisting skilled fundraising consultants can usher in an era of financial prosperity, enabling a museum to fully tap into what is often its strongest revenue stream. It is important to note that this figure does not include in-house staff.

5. Other Expenses

The myriad of other expenses, from the mundane to the unforeseen, collectively dictate the museum’s operational efficacy. Vigilant oversight and proactive management of these expenses are critical in maintaining the museum’s fiscal health and operational excellence. This category collects most of the expenses for exhibitions, programs, publications, events, and activities for history-focused organizations.

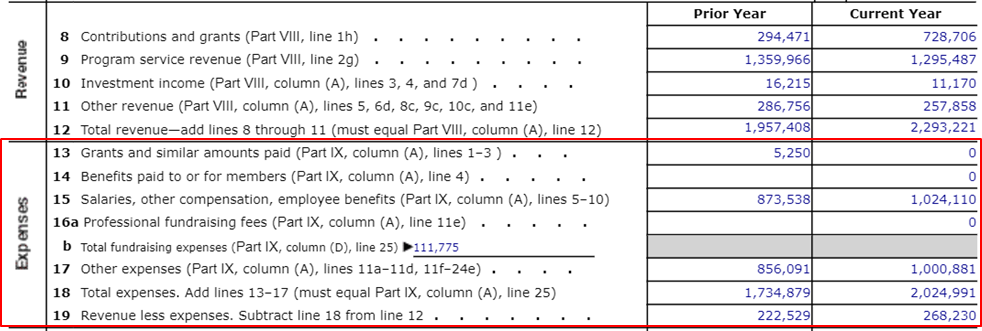

How Expenses Are Displayed in the Form 990

Insight into Expense Trends

Deeper analysis of these expense trends is hindered by the data source for our Financial Mapping Project. The National Center of Charitable Statistics (NCCS), which has a wealth of accessible non-profit financial data, has much more complete information available on revenue than expenses. We reached out to NCCS to inquire about why expense information is more limited but we did not receive a response. Because of this, our analysis can delve more deeply into revenue trends while it is more limited for expenses. The only information we can access is total expenses, compensation of officers/directors/trustees/key employees, other salaries, payroll taxes, and professional fundraising fees. We do not have access to any data on expenses for grants and similar amounts paid, benefits to or for members, total fundraising expenses, non-officer compensation, pension plan accruals and contributions, and other employee benefits.

For history-focused organizations, particularly smaller institutions, there are really only two types of expenses on the IRS Form 990 that matter: “salaries and benefits” and “other expenses.” A review of fifteen history-focused organizations showed that only three had expenses for grants, benefits paid to members, or professional fundraising fees. Furthermore, the combined average percentage accounted for by these three categories was merely 4%. For smaller institutions, the budget is typically divided between payroll, which consumes slightly more than half, and the remaining funds are allocated towards “other expenses.” A deeper understanding of these categories can help you understand how to approach your financial planning.

Salaries and Benefits

For small museums, effectively managing payroll expenses is a key aspect of financial stewardship. Payroll, often the largest category in a small history-focused organization’s budget, demands a nuanced approach that balances fiscal responsibility with the need to attract and retain competent staff. Small museums must acknowledge the reality that while their budgets are limited, the success of their operations hinges significantly on the dedication and expertise of a small pool of employees. With staffing being constrained by payroll, it is important to remember that not all manpower comes from paid individuals and weekend volunteers. The board should consider what skills and resources that they possess and can contribute to their organization. They should also have a strong understanding of the scope of their mission and the level of staffing needed to achieve it.

One common approach to maximizing the impact of payroll expenses is to diversify staff roles, blending full-time, part-time, and volunteer positions. For a small institution adding even a single full-time staff member can be a huge financial ask. This model offers flexibility in managing payroll costs while ensuring that critical functions are adequately staffed. For instance, roles requiring specialized skills or continuous oversight might be filled by full-time employees, whereas tasks with more flexible timelines or lesser demands could be allocated to part-time workers, students, or volunteers. Consultants can play a crucial role if you have a temporary need, but cannot permanently expand staff. This can come into play when doing strategic planning for a five-year plan or preparing a multi-year fundraising campaign. This approach not only curtails expenses but also creates a dynamic work environment that can adapt to changing needs and opportunities.

Additionally, small museums should be clear about job descriptions and expectations while exploring compensation models that take into account why they might be attractive to potential employees of different stripes. Understanding that competitive salaries might be challenging, institutions can offer alternative benefits such as flexible work schedules, letting employees more deeply shape the role they inhabit, or title promotions that accurately reflect the large range of responsibilities the small museum employee may have. Different incentives motivate different types of employees. It is okay to understand that you might be a stepping stone for a young museum professional just starting their career. Think of how you can retain them for as long as possible while activating the full potential of their energy and ideas for the institution. It is also okay to opt for older more established professionals for certain positions if stability would pay a premium for your institution and you lack the bandwidth for intensive training. For a small organization every time a position opens up it is an opportunity to transform your organization. Understand the needs of each role and what type of employee to invest in for maximum return for your institution’s payroll expense.

It’s also important for these museums to engage in regular financial reviews, ensuring that payroll expenses align with their operational goals and financial realities. Strategic planning should include considerations for scaling staff levels up or down in response to fluctuating funding and programmatic needs. Ultimately, the goal for small museums is to view payroll not as a mere expense but as an investment in human resources that are vital to their mission. By adopting a strategic and flexible approach to payroll management, institutions can maximize their impact while maintaining financial solvency.

Other Expenses

Managing fixed and variable expenses is a critical aspect of financial stewardship for any museum. The “other expenses” category, as illustrated in the word cloud below, encompasses a blend of these costs, each requiring distinct management strategies. Fixed expenses, like insurance or depreciation, are predictable and consistent. They represent the baseline operating costs that don’t fluctuate significantly over time. As such, they should be accounted for in a museum’s core budget, ensuring that these essential expenditures are always covered. On the other hand, variable expenses such as advertising or travel costs are more fluid. These costs can vary significantly from month to month and offer greater flexibility. Effective management of these expenses involves closely monitoring them against the museum’s current financial performance and strategic goals.

In periods of financial constraint, variable expenses can be adjusted more readily. For instance, advertising budgets can be scaled back, or alternative, less costly marketing strategies can be employed. Travel expenses can also be minimized by prioritizing essential trips or leveraging virtual meeting technologies. However, it’s important not to view these variable expenses solely as where cuts can be made for “free money”. When financially viable, investing in targeted advertising or essential travel can yield substantial benefits, enhancing the museum’s visibility, network, and operational effectiveness. Making adjustments in these “other expenses” variable costs is much less painful than attempting to make adjustments in payroll that impact your human talent, especially for smaller history-focused organizations where cutting even a single staff member could remove a quarter or a third of your institutions working hours and severely socially destabilize the operation. This is not to say you should never let staff go, sometimes it may be necessary and it is not a light decision, if someone is a poor fit or has negative externalities that impact their coworkers it may be right to make this difficult decision.

Balancing these fixed and variable expenses requires a nuanced understanding of the museum’s financial health and strategic priorities. Regular financial reviews and adaptable budgeting are key to this balance, enabling a museum to maintain its operational integrity while remaining agile and responsive to changing financial circumstances. This was the reality for many institutions during the recent COVID-19 pandemic. You never know what the next crisis may be, so a baseline level of flexibility can help protect your institution. This approach ensures that a museum can sustain its essential functions while also capitalizing on opportunities for growth and development.

The Balancing Act: Revenue and Expenses

Expenses and revenue for museums should generally align, often resulting in small annual surpluses or deficits. As non-profits, museums are not driven by excessive financial gains but rather aim to provide services that maximize impact sustainably. In managing the finances of small museums, maintaining a balance between revenue and expenses involves a dynamic challenge, requiring not just static equilibrium but continuous adjustment and strategic foresight, blending reactive and forecasting-based budgeting.

Forecasting allows museums to anticipate future revenues and expenses using historical data and market trends. This approach aids in planning for fixed costs and long-term strategic decisions. Conversely, reactive budgeting is crucial given the unpredictability of funding sources like donations and program fees. It enables museums to adjust expenditures in response to immediate financial shifts, aligning variable expenses with fluctuating revenues.

Museums must navigate diverse revenue streams, from fundraising to program fees and investment income, each with its unpredictability. Likewise, expenses range from fixed operational costs to variable ones like special exhibitions. Adaptive financial planning, incorporating both forecasting and reactive budgeting, is vital. This strategy allows for agility in spending adjustments in response to revenue changes and is crucial for building financial reserves. Reserves provide stability against revenue downturns, enabling museums to manage lean periods without compromising their mission.

Ultimately, the goal is long-term sustainability, making decisions that consider future impacts while managing present realities. By blending forecasting with reactive budgeting, museums can ensure they remain vibrant community contributors for years to come.