Organizing the “Big Tent” of the Museum Field

Imagine taking a road trip to visit Independence Hall. It would be impossible to get there if you don’t know where you are (are you starting in Boston? Chicago? Los Angeles?). Yet most museums and historic sites find themselves in this same predicament—but they don’t know it.

Knowing your museum’s financial position within its larger context can more clearly improve performance. We’ve witnessed how demographic shifts, a global pandemic, and social issues have affected all museums in the last year. Identifying which museums are responding well or poorly is largely based on rumor and anecdote, resulting in an incomplete picture of the field—and potentially misleading if a museum bases its decisions on them. Instead, we are following the advice of Karen Berman and Joe Knight, authors of Financial Intelligence (2013): “The art of accounting and finance is the art of using limited data to come as close as possible to an accurate description of how well a company is performing.”

Thanks to the availability of financial data from the Urban Institute’s National Center for Charitable Statistics (NCCS), Engaging Places will help history museums and historic sites better identify their peers and their position among them. Armed with this information, organizations can do more than benchmark against previous years. Museums will be able to financially position themselves geographically and by museum type. They will be able to evaluate their performance against their financial peers to identify strengths and weaknesses. By understanding their position, they can move forward with greater confidence.

Assisting with this endeavor is Colin Gliniecki, who recently received his master’s degree in Museum Studies at George Washington University and his bachelor’s in both Business and History from Indiana University. He has managed and analyzed development data for the National Society of Colonial Dames of America and has spent time with the National Air and Space Museum, Shedd Aquarium, the Chicago History Museum, Children’s Museum of Indianapolis, the Glenn A. Black Laboratory of Archaeology and is now tackling this national data on museums for Engaging Places.

The American Alliance of Museums takes the “big tent” approach to defining museums: “if an organization considers itself to be a museum, it’s in the tent.” (AAM 2008, 3) The Engaging Places Financial Mapping Project (EPFMP) takes a similar approach, allowing for a wide array of institutions to fall under the umbrella. Allowing so many institutions into this “tent” has its benefits, but it also can create confusion. Without a more detailed understanding of what’s inside the tent, you may be comparing yourself to institutions that don’t have meaningful similarities to you (e.g., local house museum vs. George Washington’s Mount Vernon or “apples vs. oranges”). The unfortunate reality is many boards and staff members rely on inappropriate comparisons (why can’t we be like Colonial Williamsburg or Mount Vernon?), resulting in unreasonable expectations, mission creep, unnecessary risks, and unstable finances. The Financial Mapping Project will help museums make better decisions during planning and evaluation, and ultimately increase their sustainability and impact.

To begin our “apples vs. apples” analysis of museums, we rely on how organizations are identified by the Internal Revenue Service in the Form 990, 990-EZ, or 990-PDF according to National Taxonomy of Exempt Entities (NTEE) codes. For example, art museums are identified as A51 and history museums are A54. Not only do NTEE codes define the museum field according to a national standard, but they also allow us to deconstruct it into subsets of museum types for greater clarity. Although most museums have made their financial data available for years through the Form 990, the data has not been analyzed meaningfully to understand the shapes, trends, and behaviors of the different corners of the field.

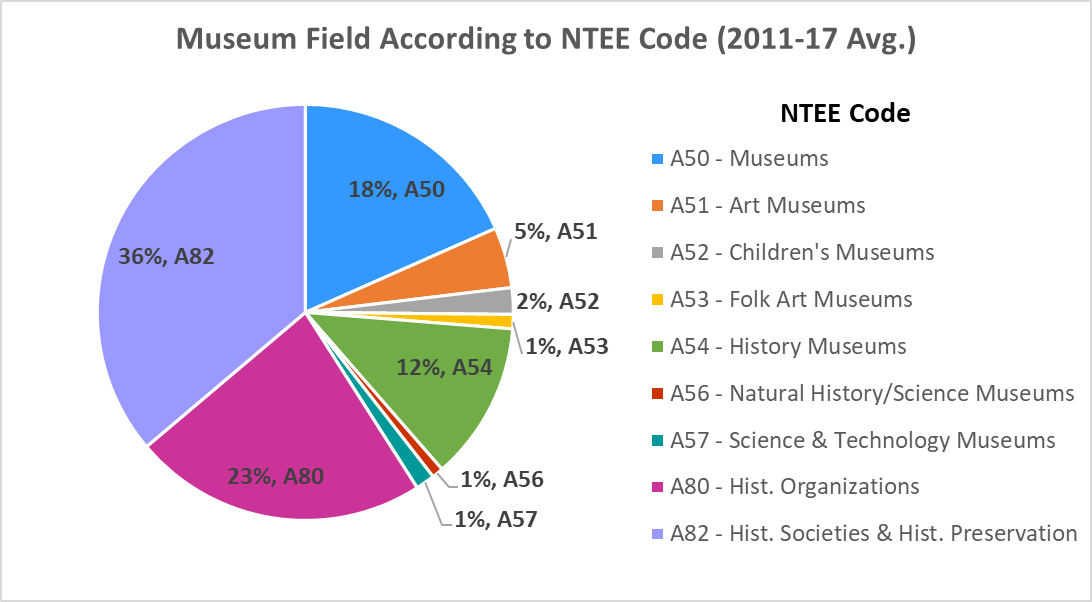

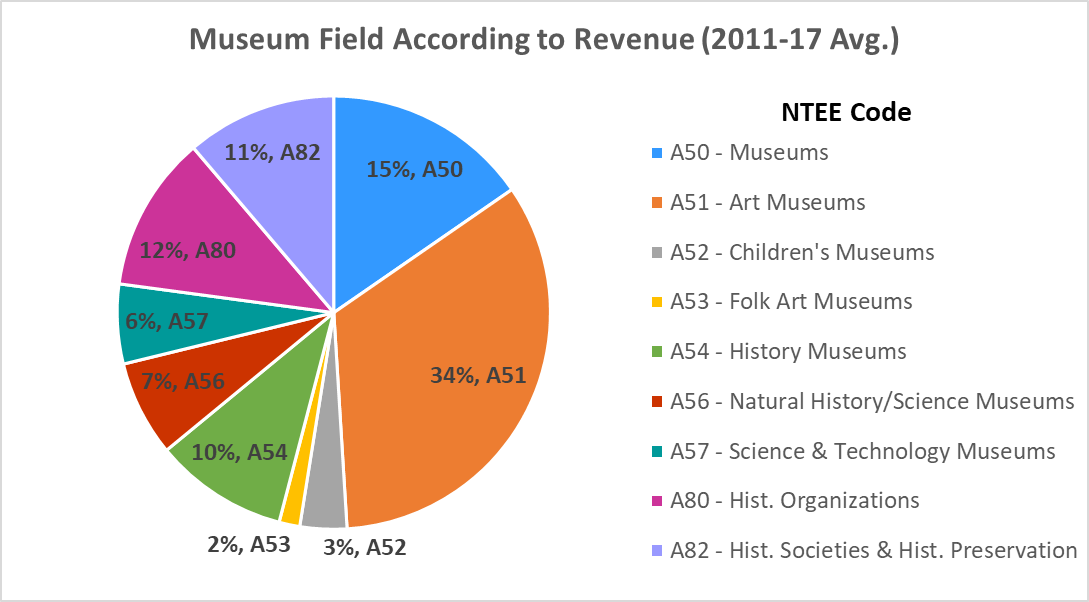

The two charts below illustrate how an analysis by NTEE codes can help museums gain a clearer perspective of their peer institutions. Figure 1 shows the composition of the museum field according to type (e.g., art vs history), while Figure 2 displays the field by combined revenue per type (e.g., total revenue for art museums vs history museums). Art Museums (A51 in orange) represent 5 percent of the museum field, yet attract 34 percent of the revenue. By contrast, Historical Organizations (A80 in magenta) and Historical Societies & Historic Preservation (A82 in violet) collectively represent nearly 60 percent of the museum field but only capture 20 percent of total revenue? Is this suggesting history organizations are becoming less financially sustainable? Which museums have successfully broken this national pattern and have managed steady growth?

Figure 1. Source: Internal Revenue Services and NCCS

Figure 2. Source: Internal Revenue Services and NCCS

In the coming months, Engaging Places will post a series of articles analyzing museums by type, region, and over time with our recommendations. These articles will investigate what the average institution in these museum types looks like and which direction these museum types look to be heading.

Methodology

In late 2020, Engaging Places began compiling museum data from the Urban Institute’s National Center for Charitable Statistics (NCCS). NCCS collects data from the Internal Revenue Service on charities, foundations, and 501(c) organizations that is publicly available as IRS Forms 990, 990-EZ, or 990-PDF. This data is freely available individually or in bulk from the Internal Revenue Service and the National Center for Charitable Statistics.

Our analysis is based on two datasets: a General Museum Dataset and a Specialized Panel Dataset. The first has more than ten thousand museums from all 50 states and Washington, D.C. for each year from 2011 to 2017 representing more than ten billion dollars in revenue. This “General Museum Dataset” allows for snapshots of the museum field’s performance and industry averages. To prepare for our analysis, we adjusted and validated the data to provide the best possible consistency over time and across the field, which is not possible through an analysis of individual financial reports (if it were even possible to obtain them).

When we perform an analysis by museum type, we rely on how organizations are identified in the Form 990 according to National Taxonomy of Exempt Entities (NTEE) codes (details below). A house museum, for example, may be identified as a Museum (NTEE code A50), History Museum (A54), or Historical Society & Historic Preservation (A82). Each group is distinct and there are no sub-sets, so if a museum is identified as a History Museum (A54), they are not part of another group, such as Museum (A50) or Historical Organization (A80).

Because fiscal years will not align, when we perform an analysis by date, we group data by calendar year to provide the best comparison possible. For example, the 2017 data will include museums with fiscal years ending June 30, 2017 and museums with a fiscal year ending December 31, 2017. Although the data we present is five years old or more, it is the latest data available due to preparation and processing by the filers and IRS.

When we perform an analysis over time, we only include organizations that appear every year from 2012 to 2016, a smaller dataset which we refer to as “Specialized Panel Dataset”. We omitted institutions that may have entered or left the field during this period, or organizations with revenues below $50,000 (IRS Form 990-N). We recognize this excludes very small organizations and some larger ones, however, we believe this dataset of 5,997 institutions from 2012 to 2016 still provides the best data available for conducting a panel data analysis over several years.

To provide useful comparisons for history-related institutions working within similar structures, laws, and practices, we excluded Zoos and Aquariums (D50) and Botanical Gardens & Arboreta (C41) museums that primarily care for living collections or are operated by organizations based outside the United States. These institutions represent less than 1.5% of the museum field. Finally, museums operated by government agencies (such as the Smithsonian Institution or state agencies) or parent organizations (such as universities or regional associations) are excluded because they do not file annual reports with the IRS (although their “friends” or support organization may). At times outliers are excluded from our data. When this is required we work to eliminate the 5% most extreme outliers using the interquartile range of the relevant data.

National Taxonomy of Exempt Entities (NTEE) Code Categories and Definitions

A50 Museums: Organizations that acquire, preserve, research, exhibit and provide for the educational use of works of art, objects or artifacts that are related to the study of zoology, biology, botany, mineralogy, geology and other natural sciences; history; archeology; or science and technology.

A51 Art Museums: Organizations that acquire, preserve and exhibit collections of objects including fine art, decorative art, folk/ethnic art and textiles that are collected primarily for their aesthetic qualities and their importance as representatives of a particular artistic tradition or style.

A52 Children’s Museums: Organizations that develop and maintain educational exhibits that are structured for the size, interests and intellectual capacity of young children. Children’s museums are participatory and allow visitors to interact with the exhibits (touching, exploring, manipulating), and many offer organized lessons for groups of school children that focus on one or more of the exhibits. NOTE: See also A57, Science and Technology Museums, for other organizations with substantial activities and collections for children.

A53 Folk Art Museums: Specialized museums, foundations and other organizations whose activities and collections preserve and promote the culture and history of a specific nationality, or racial or ethnic group, e.g. Native Americans.

A54 History Museums: Organizations that acquire, preserve, research and exhibit collections of objects including documents, tools, implements and furnishings that have significance in helping to interpret or understand the past. History museums may specialize in a specific era such as early Greece or Rome, a particular geographical region such as California or Appalachia, a particular ethnic or cultural group such as Native Americans or a specific subject area such as costumes; and may contain items created or used by contemporary or historical figures.

A56 Natural History & Natural Science Museums: Organizations that acquire, preserve, research and exhibit collections of objects that have significance in the natural sciences including botany, zoology, geology and physical and cultural anthropology.

A57 Science & Technology Museums: Organizations that develop and maintain educational exhibits which illustrate principles from mathematics and the physical sciences.

A80 Historical Organizations: Organizations that promote awareness of and appreciation for history and historical artifacts.

A82 Historical Societies & Historic Preservation: Organizations that sponsor activities which celebrate, memorialize and sometimes recreate important events in history such as battles, treaties, speeches, centennials, independence days, catastrophes that had an important impact or other similar occasions.

References

American Association of Museums. National Standards and Best Practices for U. S. Museums. Washington, DC: American Association of Museums, 2008.

Berman, Karen and Joe Knight. Financial Intelligence, Revised Edition. Boston: Harvard Business Review Press, 2013.

Jones, Deondre. “National Taxonomy of Exempt Entities (NTEE) Codes.” National Center for Charitable Statistics, April 2, 2019.

Magretta, Joan. Understanding Michael Porter: The Essential Guide to Competition and Strategy. Boston: Harvard Business Review Press, 2012.

Zimmerman, Steve and Jeanne Bell. The Sustainability Mindset: Using the Matrix Map to Make Strategic Decisions. San Francisco: Jossey-Bass, 2015.