In the colorful tapestry of history-focused organizations, every thread of revenue has a role to play in the success of the organization. Perhaps the most unique collection of these threads is the “Other” revenue category. This singular “Other” thread houses a miscellany of revenue sources that don’t fit into the categories of “Investment Income”, “Program Service Revenue”, and “Contributions and Grants”. At first glance, this classification may appear insignificant, yet it often proves to be a silent contributor that underpins the fiscal health of History-Focused Organizations [Museums (NTEE A50), History Museums (A54), History Organizations (A80), and Historical Societies & Historic Preservation (A82)].

Understanding this “Other” revenue can be like deciphering an ancient dialect. It is made no easier by the fact that IRS Form 990 at times uses the terms revenue and income interchangeably. While some categories of this revenue such as royalties and inventory sales may be familiar, “miscellaneous” often contains difficult to parse odds and ends such as third-party events, insurance proceeds, ATM fees, and revenue from hosting satellite towers. Most often this miscellaneous revenue is unspecified and simply named “miscellaneous” or “other” which can make it difficult to get the full picture of a particular institution’s revenue sources. We advise limiting the classification of your total revenue as “miscellaneous” to no more than 1%. While judicious use of this category can help define your other revenue streams more clearly, overuse could lead to a lack of clarity about a significant portion of your revenue. It is crucial to maintain a comprehensive understanding of your financial situation.

Avg.) Source: Internal Revenue Service and National Center for Charitable Statistics.

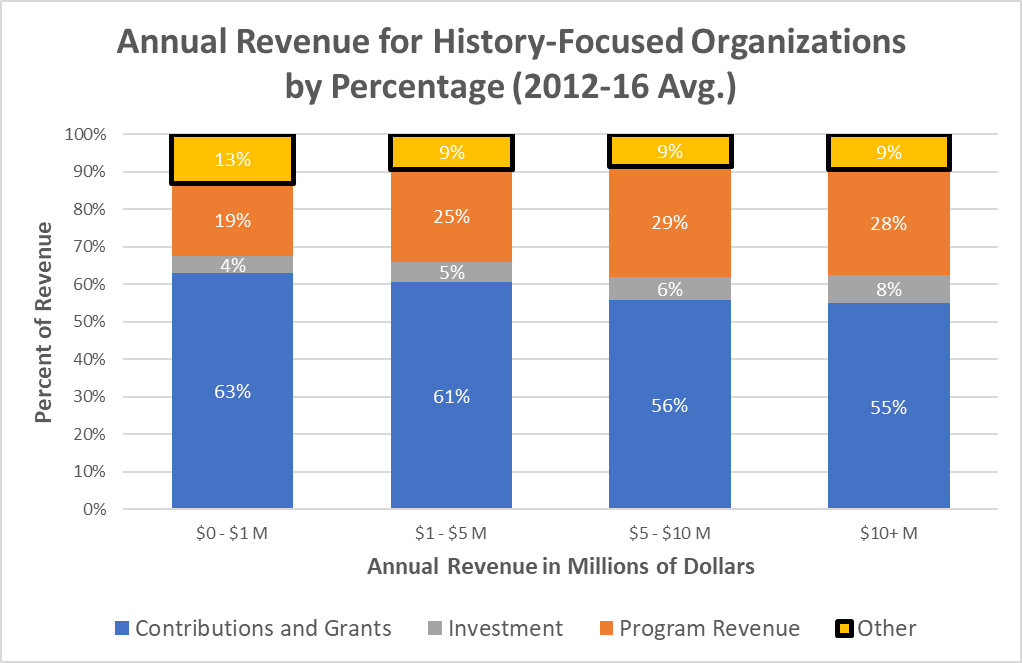

As history-focused organizations develop, their revenue stream doesn’t follow a linear pattern of growth or reduction. Instead, it evolves in a unique, non-linear manner. For institutions operating on $1 million or less in revenue, “Other” makes up 13% of all revenue, from there it plateaus at 9% for institutions of all larger sizes. However, this dip and subsequent plateau do not paint the full picture of this peculiar revenue stream. The individual components of this stream continue to evolve, some growing more important as the institution grows and others diminishing. For example, special events are quite important to organizations operating on less than $1 million in revenue each year while for larger organizations this importance plummets. Contrarily, the sale of inventory revolving around gift shops, continues to grow in relative importance as institutions grow larger in size.

This subtle evolving nature makes “Other” revenue a fascinating study, and yet, one should not mistake it as a main source of funds. Instead, consider it as a supplementary tributary that feeds into your primary river of revenue. It bolsters your financial standing and often contributes to mission-aligned endeavors that augment your institution’s commitment to preserve, interpret, and share valuable historical narratives.

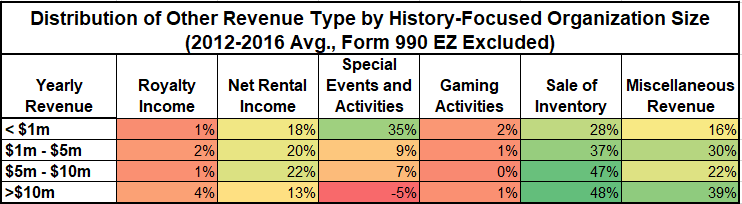

A myriad of avenues can lead to the generation of “Other” revenue, often providing a blend of monetary and non-monetary benefits, contributing to both your organization’s financial and social capital. Navigating the “Other” revenue landscape necessitates a keen understanding of your organization’s ecosystem and is highly situational. Some possibilities make strong sense for one institution but are completely unfeasible for others. In Figure 2 above, see how the reliance on some “Other” revenue streams shifts and changes depending on the size of the organizations. Just because another history-focused organization is able to cultivate a revenue stream doesn’t mean it’s inherently an opportunity for you.

Consider, for instance, the humble museum gift shop. While it may not be a consistent generator of revenue for all institutions, it can be quite effective in high-traffic locales. Beyond its monetary value, a gift shop serves as an ambassador for your organization, offering visitors tangible memories that remind them of their experience. As such, a museum gift shop is not merely a commercial outlet, but an extension of the museum experience that helps to extend the organization’s influence beyond its physical boundaries. The Field Museum in Chicago has the scale to host a museum gift shop in O’Hare International Airport, while a smaller institution might try to host an outpost at their weekly local farmers market.

Then there’s the opportunity for licensing and royalties, a potentially lucrative avenue for organizations blessed with exceptional collections or a renowned brand image. A case in point is the National Trust for Historic Preservation and Historic New England, which turned their brand recognition into a successful business venture by licensing bespoke paint colors. However, licensing often involves intricate legalities, making it a path best navigated by larger, well-resourced organizations.

A significant advantage for many history-focused organizations is the ownership of historically significant or visually captivating properties. These can be rented out for events such as weddings, corporate gatherings, or film shoots. Site rentals, therefore, can become a considerable revenue stream. Additionally, functional opportunities could include parking fees, installing cell towers, or housing ATMs, thus leveraging property assets to generate a steady revenue stream. In 2017 parking and guest services fees alone generated $2.3 million in revenue for the Museum of Science and Industry in Chicago.

Significant “Other” revenue sources are not restricted to large, well-established institutions. Small organizations, with a sharp understanding of their strengths and unique offerings, can successfully tap into this revenue stream. As organizations grow in scale some revenue opportunities may change into opportunities to focus on mission. Notice how in Figure 2 above special events and activities generate funds for small organizations but become an expense for larger ones who may be focusing on celebrating and stewarding with these events rather than monetizing them.

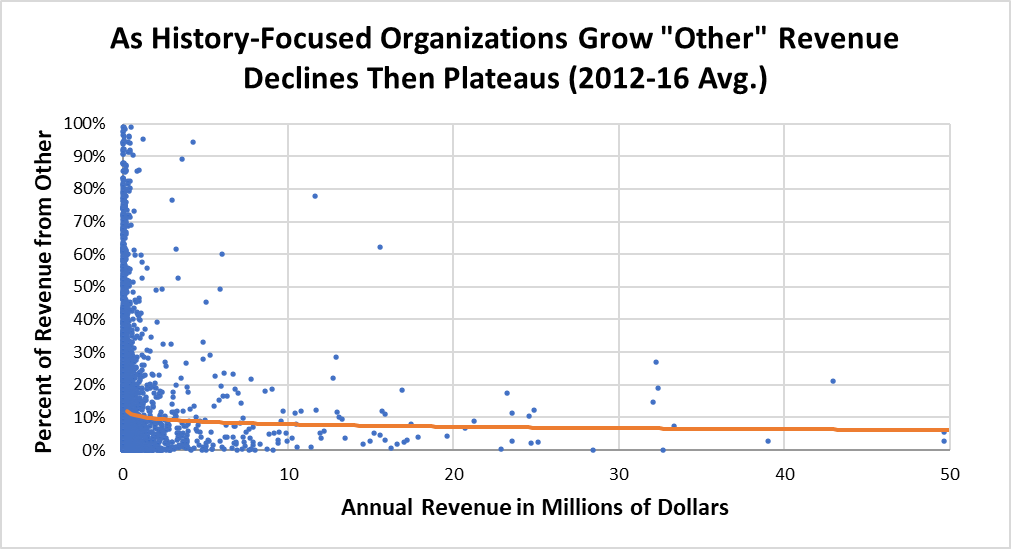

However, don’t let the pursuit of “Other” revenue overshadow your primary mission. It should act as a support structure, bolstering your mission and values, not an overbearing entity that distorts your focus away from the organization’s core purpose. The secret lies in striking a harmonious balance. A diversified revenue portfolio that underpins your mission while bolstering financial stability. Smaller organizations may be more likely to be funded disproportionately by more unusual revenue streams that fall in the “Other” category that fit their early life cycle circumstance (see Figure 3 above). However, this revenue should decrease in relative importance as more traditional fundraising and program infrastructure is created and begins to play a role in an organization’s finances.

In essence, the “Other” revenue category, while enigmatic, is a powerful testament to the innovative and diverse ways museums can generate revenue. It’s a symbol of the sector’s scrappiness at times, particularly for small organizations on shoestring budgets. As history-focused organizations continue their journey through the economic landscape, the “Other” revenue stream will undoubtedly continue to play an integral, albeit somewhat mysterious, role in their financial strategies.

References

Hay, L. E. and Wilson, E. R. Accounting for Governmental and Nonprofit Entities, Tenth Edition. Chicago: Irwin, 1995.

Museum of Science and Industry. “Form 990.” Chicago: Museum of Science and Industry, Fiscal Year Ending December 2017.

Thomas, L. “Guide to Period Paints.” Old House Journal Magazine, June 17, 2021. https://www.oldhouseonline.com/repairs-and-how-to/guide-period-appropriate-paints/